Martin's 'how to slash all debt costs' January masterclass

Can't afford to clear your debt? You can't afford not to try to move it to 0% - save £1,000s

Cards, mortgages, overdrafts, loans, store cards, BNPL and more

Debt is a problem right now. It is often depressing, dangerous and debilitating. Tackling it may take a deep breath, but leaving it to fester is not an option - the interest will keep accruing and things will get worse.

The priorities are to stop borrowing more (or you risk a debt spiral) and to try to reduce the interest you're paying. That way more of your repayments clear the actual debt rather than just cover the interest, so you can be debt-free quicker.

So it's time for my annual interest-cutting masterclass. From loans to mortgages to buy now, pay later - it's more important than ever in this year with millions of people's finances hit by the pandemic.

A balance transfer (BT) is where you get a new card to repay debt on your old cards, so you owe it instead but at 0%. While 0% lengths are shorter than a few years ago, there are some pretty decent newly-launched deals right now, though we're not sure how long they'll last.

- DON'T just apply. First, find which cards will accept you. Our BT eligibility calc shows your acceptance odds for most of the top cards, helping you to minimise applications and protect your credit score - crucial as many lenders have tighter acceptance criteria currently.

It works, as MoneySaver Frank emailed: "Half my £300/mth card payment was swallowed up in interest. After reading Martin's article, I immediately used your eligibility calculator and within a few minutes I'd been accepted for new, long-term 0% interest. Thank you so much."

- Go for the lowest fee (incorporating cashback) in the time you're sure you can repay. Unsure? Play safe and go long. Here are our current top pick new customer BT deals.

Always follow the Balance Transfer Golden Rules:

a) Never miss the min monthly repayment.

b) Clear the card before the 0% ends, or you pay the higher APR.

c) Don't spend/withdraw cash. It usually isn't at the cheap rate.

d) Usually you must transfer within 1-3mths to get the 0% deal - check.

e) You can't transfer between two cards from the same banking group.

Full help and info in Best Balance Transfers (and see APR Examples).

Covid help: If you are struggling financially due to the pandemic, you can request a credit card payment holiday, but only do it if needed as interest still mounts up.

Store cards are just credit cards you only use in one store chain, but usually with far costlier interest, eg, New Look is 28.9% rep APR, Argos 29.9%. But you can balance-transfer store card debt too, so just follow the help above.

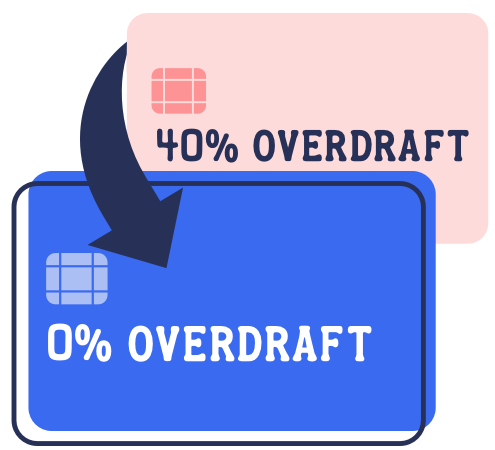

Many people think credit cards bad, debit cards good. Not if you're overdrawn - almost all major banks now charge about 40% for overdrafts, double even a high street credit card - making them a serious danger debt. If you're paying that, take action. See 10 Overdraft Cost-Cutting Tips , but here's the key info...

Many people think credit cards bad, debit cards good. Not if you're overdrawn - almost all major banks now charge about 40% for overdrafts, double even a high street credit card - making them a serious danger debt. If you're paying that, take action. See 10 Overdraft Cost-Cutting Tips , but here's the key info...

a) Ends 31 Jan. £500 0% overdrafts if struggling financially due to Covid. Banks are no longer required to give official Covid-related 0% overdrafts, but Lloyds, Bank of Scot, Halifax and Santander do; with 3mth-long up-to-£500 0% on request until 31 Jan for those struggling. With other banks, if keeping afloat is tough, speak to them as many can offer help. Full info & how to apply in Covid overdraft help.

b) Switch to a 0% overdraft. If you can't get or aren't due the help above, or want 0% for longer, many accepted newbies to First Direct* and M&S Bank get an ongoing £250 0% overdraft - great if you owe a smaller amount.

Alternatively, Nationwide FlexDirect* offers some a bigger 0% overdraft for a year, though the size depends on your creditworthiness. So see this as respite and aim to clear before then. With all these, go over that limit and it's 39.9% EAR variable. Full info and eligibility help for all of these in top overdraft accounts.

c) Use a 0% money transfer credit card. For larger overdrafts, a few specialist cards also allow 0% money transfers for up to 18mths - where the card pays cash directly into your bank account, clearing your overdraft, so you owe it instead.

It can be a big help, as Tricia emailed: "Had a £3,000 overdraft, so I took advantage of a 0% money transfer at a one-off 1.9% fee. The account is now in credit and the card will be cleared in 12mths. Result."

If you've a loan, can you get a new one to clear it and pay less? As MoneySaver Sean emailed: "Two years ago, we took out an 11.9% loan. After reading your guidance, we got a new 5.9% loan to pay it off, saving £2,164 in interest. Wouldn't have had the confidence without you. Thanks."

This one's trickier though, as it's not just about getting cheaper APRs. Full help's in Cut existing loan costs, but here are my quick steps (shall we dance) to check...

- STEP 1: Ask your current lender for a 'settlement figure'. Ie, how much it'll cost to clear your current loan, including any early repayment costs (which tells you how big a new loan you'll need to get to clear it).

- STEP 2: Find the cheapest loan for the settlement figure - and if you can actually get it. Our Loans Eligibility Calc shows your odds of acceptance for many loans, and that's the best route.

The current cheapest rates incl Hitachi* 8.4% for £3k-£5k, Tesco Bank* 3.4% for £5k-£7.5k, Cahoot* and TSB* 2.8% for £7.5k-£15k. More in cheapest loans. For loans under £3,000, 0% money transfer cards are usually cheaper.

Yet do be warned all these loan rates are 'representative APR', meaning sadly only 51% of accepted customers need get that rate.

- STEP 3: Find out if a new loan's cheaper than your current one. Multiply your monthly repayments by how many months you have left (ask the lender if you don't know) to find how much you'll pay if you stick, then plug all the figures into the MSE Loan Switching Calc.

Covid help: If you are struggling financially due to the pandemic, you can request a loan payment holiday, but only do it if needed as interest still mounts up.

The UK base rate is at a record low 0.1%, and that has an impact on mortgages, so this should be the perfect time to find a cheaper deal. The problem is, for those with little equity in their home, (ie, your mortgage is a high proportion of your home's value) many mortgages have been pulled.

The UK base rate is at a record low 0.1%, and that has an impact on mortgages, so this should be the perfect time to find a cheaper deal. The problem is, for those with little equity in their home, (ie, your mortgage is a high proportion of your home's value) many mortgages have been pulled.

Yet it's still worth everyone checking, as the very cheapest rates are down at 1.05% for 2yr fixes and a stunning 1.29% 5yr fix. So if your mortgage deal's near ending, or already has, check. As Helen emailed: "I remortgaged - the rate changed from around 5% to 1.48% fixed for 5yrs. This equates to a saving of £45,000 over the 5yrs. Thanks to your site." Here are four quick tips to help:

a) Grab my free 66-page remortgage booklet (or 1st-time buyers' booklet).

b) Benchmark your cheapest rate using our Mortgage Comparison tool.

c) Consider using a mortgage broker to find the best deal, as they have information about acceptance chances not available to the public.

d) Use the Ultimate Mortgage Calculators to work out savings, compare deals, see the gain from overpaying and more.

Covid help: If you are struggling financially due to the pandemic, you can request a mortgage payment holiday, but only do it if needed as interest still mounts up.

Mortgage prisoner? MSE and I are still campaigning on this. I recently met the Treasury Minister responsible to discuss it - see our Mortgage prisoners need Govt help MSE News story for the latest.

You can't cut costs from interest free, so this is just a warning. Klarna, Clearpay, Laybuy and other buy now, pay later (BNPL) firms have rapidly become a near-ubiquitous way to pay at many online retailers, offering to spread the cost over a few weeks or months.

While there's no interest, if it goes wrong, you can face late fees, marks on your credit file or even bailiffs. These firms make money because they're so good at tweaking our spending nipples to make us want to buy more and more. So be very careful.

Worse still, BNPL is unregulated, so you've few rights if things go wrong, and you can't take them to the ombudsman. This must change - see my 'BNPL must be regulated' Treasury Committee evidence.

Payday loans are an interest and financial nightmare. Try to avoid them if at all possible. If you've got them, check out our Payday Loan Help guide and, crucially, if you're struggling financially due to lockdown, you can apply to request a 1mth payment & interest holiday . Uniquely, for payday loans the interest is frozen during the holiday, so it's a good option.

If you previously had one, you may also be able to reclaim payday loans. As Jimmy, wonderfully, emailed: "Followed your guidance and contacted about a dozen payday lenders. Altogether I've now received over £7,000 back. Makes me shudder what state my finances were actually in... but your guidance helped me into a much better position. Thank you." It's also worth noting you can reclaim guarantor loans too.

Whether you're accepted for cheap deals or not, always aim to pay as much off as you possibly can, as quickly as you can (without damaging your financial stability). A few things help with this...

a) Prioritise repaying the highest-interest debt first. It grows fastest. List all debts in order of APR (highest first), then use all spare cash to clear that and just pay minimums on everything else. Once it's clear, focus on the next costliest.

With overdraft interest now so high, for many that'll mean paying minimums on your credit card to get your overdraft in credit. Really tricky to manage sadly.

b) Got savings? Use 'em to clear costly debts. Many people are emotionally attached to savings in the bank, but remember when you save, in practice that's just you giving your bank a loan. However, it usually pays you less than it charges when you borrow from it. So if the interest cost of debt is higher than you earn saving (it will be for most), pay off the debt with the savings - provided there are no penalties for doing so.

In most cases, it's worth holding back 3-6mths worth of bills in an emergency savings fund. However, with credit cards, as it's an open facility and costs a lot, you could use your emergency fund to clear it. Then if an emergency happens, borrow back so you're no worse off, but save in the meantime.

c) Do a budget and manage your money. Get control of your spending - do a budget to see where the cash is going. What really counts is how you control it - try my piggybanking system.

d) Boost your credit score. You'll be eligible for better debt cost-cutting deals in future. See my 27 ways to boost your credit score guide.

e) Debt fighting is best done with friends. You may find great inspiration in our Debt-Free Wannabe and Mortgage-Free Wannabe MSE Forum boards.

If things are tough, the solutions above about cutting costs may not be right for you. Three quick questions:

a) Are you struggling to meet your min monthly repayments?

b) Do you have non-mortgage/student loan debt over a year's salary?

c) Do you have sleepless nights or depression/anxiety over debt?

If the answer is yes to any of those, instead of the solutions above, I'd get free, one-on-one debt counselling help from Citizens Advice, National Debtline, StepChange or CAP. They're there to help, not judge. The most common thing I hear after is: "I finally got a good night's sleep."

And BELIEVE THINGS CAN IMPROVE. Read inspiring stories in our Debt Help forum and also see our Mental Health & Debt guide. Full info in Debt Crisis Help.

-------------------------------------------

It's BILL BUSTER week - time to slay a few fiscal pelicans

8.30pm Thu, ITV: Martin's Money Show Live

A MUST-WATCH show this week, my annual bill buster, where we take down pelicans (big bills) - energy, broadband, water and lots more. I'll run you through how to save £100s or £1,000s without you feeling a thing.

And of course, as it's live you can tweet suggested questions to @MartinSLewis, but you must use the show's hashtag #MartinLewis. Do tune in or ask a friend to transcribe on papyrus.

No comments:

Post a Comment